In Part 1 of our blog series, Playing the Long Game, we discussed the importance of taking a population-based approach to care management. An important concept within this framework is managing risk at all levels of the population through wellness promotion, prevention, and slowing the progression of disease. Because risk is such a huge component of functional success, we thought we’d take a minute to clarify the concepts of risk, predictive modeling, and stratification. If you don’t need this primer, stay tuned for our upcoming blog.

What do we mean when we talk about “Risk”

In the simplest form, risk is a factor of the likelihood that an event will occur and the severity/amount of loss expected to result from that event. In most industries, risk refers to financial loss. In healthcare, however, risk is often spoken about in terms of events, such as hospital admissions, emergency department visits, loss of function, or the development of a certain clinical state, such as diabetes or sepsis.

In health care, a risk score is a number that is assigned to individuals based on their demographics and diagnoses—basically a numerical representation of how costly they are expected to be in comparison to the rest of the population, or how likely they are to experience a major event.

At a very high 10,000 foot level, risk scores are calculated using age, sex, location, and diagnosis; some may even use medications as a variable. There are many models, methods, and proprietary technology out there that calculate health risk. Most of them use a combination of clinical and pharmacy claims data, only a select few use clinical data (e.g., Johns Hopkins Adjusted Clinical Grouper [ACG] system), and even less use socioeconomic and community-level information.

Risk Management is the foundation to a best-in-class population health enterprise. Understanding risk scores is key to creating efficiency and alignment across risk catpure & adjustment; quality improvement & Stars ratings [HEDIS]; and proactive care management.

How are risk scores used today?

Actuarial analysis & underwriting functions

Risk scores have traditionally been used by health insurance companies for price/premium-setting and structuring policy benefits. Actuarial analysts used them to predict the expected healthcare costs and utilization of a patient/population (pricing risk) and then quantify each member’s health relative to the rest of the population to determine expected variations from the population as well as what resources are needed to care for these patients (underwriting risk).

Provider & health plan reimbursement

Risk scores have also been used by health insurance companies and federal regulators (Center for Medicare & Medicaid Services, CMS), to normalize populations so that providers and health plan reimbursement is adjusted based on the population’s health risk. This is especially important in value-based programs when provider effectiveness is measured based on outcomes and resource utilization of an assigned panel of patients.

Program management

In recent years, risk scores have become increasingly important to providers as a means to identify and prioritize patients’ clinical needs for eligibility and enrollment into clinical care programs. It’s also used in financial modeling and resource allocation for program design so that the appropriate staffing is put in place to accommodate the needs of the patient population.

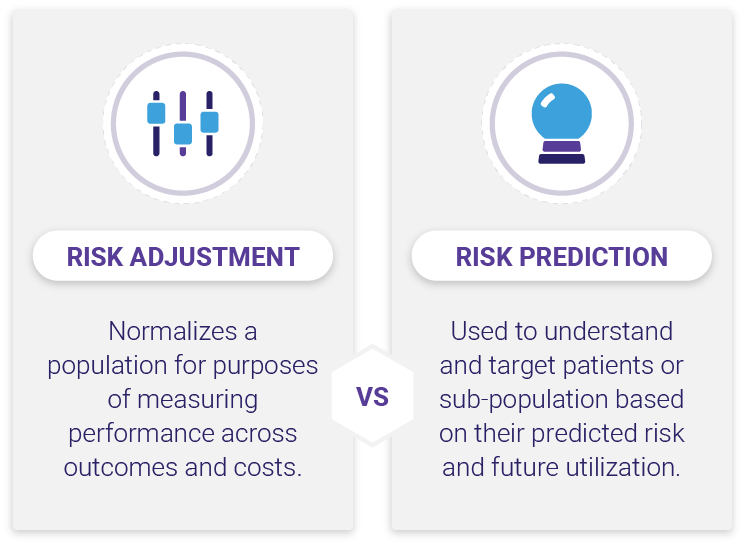

Risk adjustment vs risk prediction

When speaking about risk scores and the models used to calculate them, it’s important to understand the distinction between risk adjustment and risk prediction. Risk adjustment models are used to normalize or standardize a population for purposes of measuring performance across outcomes and costs. Risk adjustment is important for ensuring that providers who treat complex populations are not penalized under a pay-for-performance system, e.g., Medicare Advantage. A good example of this type of risk modeling is the Hierarchical Condition Categories (HCC) model used by the Center for Medicare and Medicaid Services (CMS).

Risk prediction (a.k.a. predictive modeling) on the other hand is used to identify the future risk of a patient/subpopulation. Predictive modeling is important both in actuarial analysis /underwriting functions and care management. In part 1 of this series we briefly touched on the “fluidity of risk”; the idea that members within a population will move between risk levels from one year to the next and that roughly 18 – 20% of moderate-risk patients will become high-risk patients and about 16% of the high-risk members will transition to lower-risk groups, regardless of interventions being applied (a statistical phenomenon referred to as “regression to the mean”). When planning for care management or conducting actuarial analysis it is important to be able to predict which members will remain in their risk group and which ones will transition to another risk group.

Now that we understand risk and the difference between adjustment vs. prediction, let’s talk “Stratification”

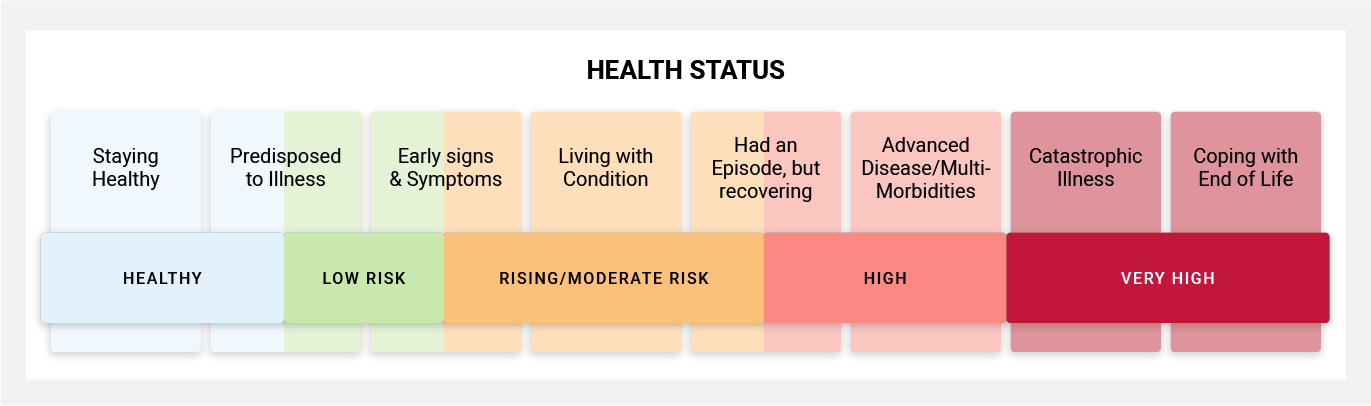

Risk stratification uses predictive modeling as a basis to assign each patient into a risk group based on health complexity and clinical care needs. One very important distinction between risk, predictive modeling, and stratification is that risk stratification combines several individual risk scores to create a broader profile of a patient.

For example at Inflight Health, we use the Johns Hopkins Adjusted Clinical Grouper (ACG) system. Using this system, we are able to look across multiple risk factors such as morbidity complexity, duration & severity of the condition, diagnosis certainty, as well as expected resources needed to treat the condition. In addition to these factors, we can look at care density risk, frailty and fall risk, risk of hospitalization, as well as biometric and polypharmacy risk markers. We’ll continue exploring stratification in our next blog. In the meantime you can contact our Success team with any questions you may have or to learn more about our solutions.